And Tita’s tooth

heritage insuranceNew York Stock Exchange: HRTG) provides property and casualty insurance for residential properties in the Southeast. Dichotomy Capital wrote one of Seeking Alpha’s most popular articles on this topic in 2016. They noted:

Headed by Bruce Lucas, the company swooped in exceptional reinsurance market by securing multi-year low reinsurance rates at previously unheard-of levels. While most advantages in insurance are fleeting, Heritage will be able to expand faster than competitors and can handle other types of business with less worry. The model for expansion into other states is plausible and has been done by several other players in the industry… Ultimately, Heritage would be an attractive candidate to acquire a larger national homeowners insurer that wants access to HRTG’s reinsurance book and profitable policies .

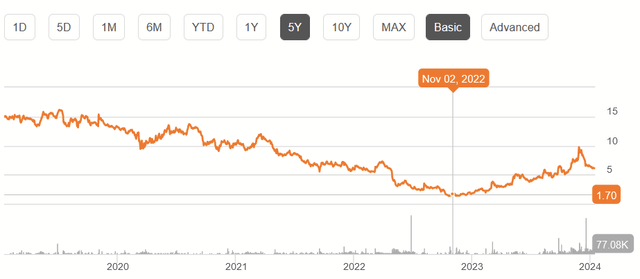

HRTG was trading at $11.94 at the time. Rocky financial results in The years that followed sent the stock price well below $2 in the latter half of 2022. Standing above $6 per share as we enter 2024, the risks and rewards are now very different. I will demonstrate that the current premium to tangible book value lacks justification (particularly for those interested in a safe, long-term compounding of value) and why current owners would be better off selling.

Business model

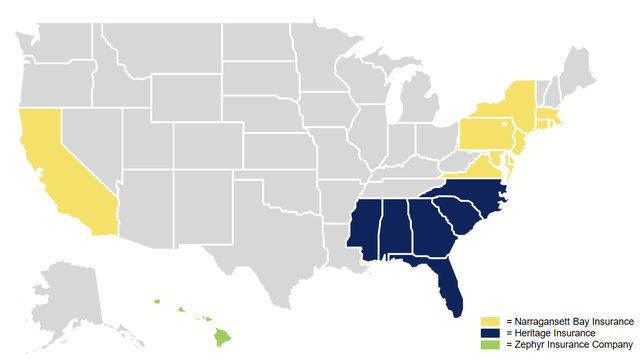

The Company’s (and its subsidiaries’) insurance business covers personal and commercial properties. It operates primarily on the East Coast.

Company presentation for the third quarter of 2023

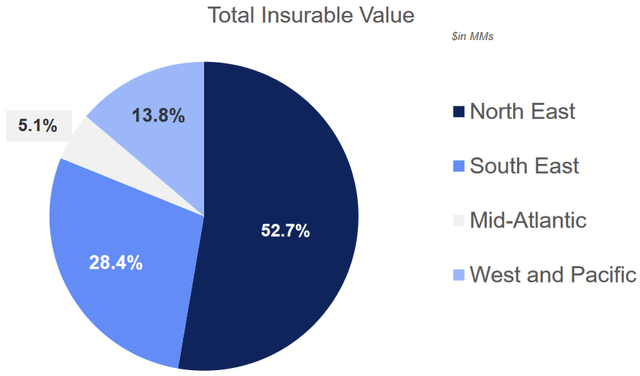

Most of their physical business is concentrated in the Northeast, but they have a significant concentration in Florida.

Company presentation for the third quarter of 2023

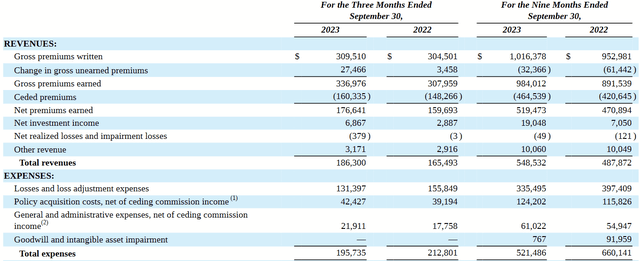

The business is to provide coverage for claims relating to residential property, a type of insurance that will probably be familiar to most readers. In addition to collecting revenue for premiums, the company has a vertical model that generates revenue from adjacent services.

Third Quarter 2023 Form 10Q

Most of its revenue comes from premiums on insurance policies written, minus the surrender of reinsurance. With the damage that can be caused by hurricanes in this region and winter storms in the north, reinsurance is an important way to mitigate their risks. However, even this could put pressure on the company. As we can see, expenses exceed revenues, and the company does not make a profit from the IPO.

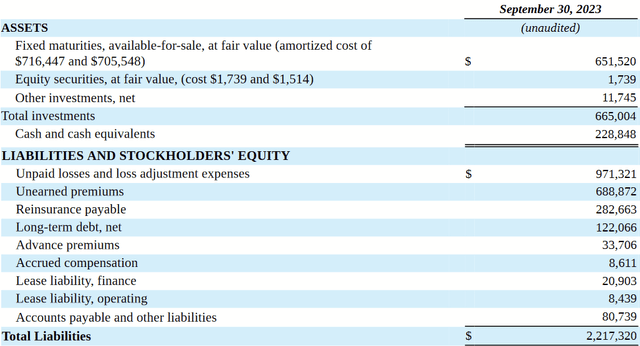

While the company reported assets of more than $2.3 billion in Q3 2023, its cash position is rather small, at $228.9 million.

Third Quarter 2023 Form 10Q

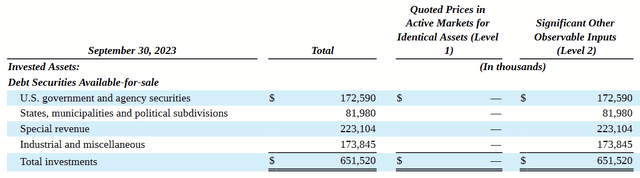

The value of the investor’s float portfolio enhancement is approximately $665 million.

Third Quarter 2023 Form 10Q

Most of this portfolio is invested in debt securities linked to the public sector. The 2022 Form 10-K explains the investment strategy:

Our investment objectives include liquidity, safety and security of capital and returns. The investment policy limits investments in common and preferred stocks and requires a minimum A-weighted average portfolio quality for our bond portfolio with an aggregate duration of three to five years. No more than 2% of accepted assets can be invested in any one issuer, with slightly higher limits for highly rated securities, excluding government-related securities. Investments in commercial real estate mortgages may not exceed 10% of accepted assets. Prohibited investments include short sales and margin purchases, oil, gas, mineral or other types of leases, speculative uses of futures and options, securities of unrated companies, securities not denominated in the United States, convertible securities, high-risk CMO instruments, and Repo and securities lending. Transactions and speculative operations in the evaluation of foreign currencies.

As such, I believe the portfolio is relatively healthy from a short-term perspective. However, the size of the liabilities (at $2.2 billion) increases the company’s liquidity limits.

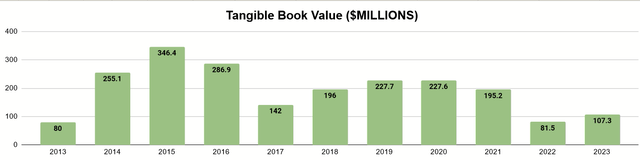

Financial history

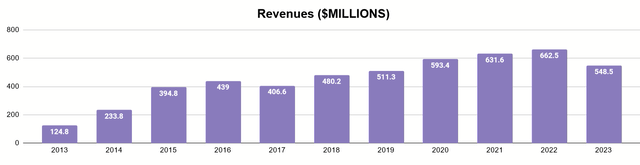

Founded in 2012 with an initial public offering in 2014, the company has a decade of financial data to give us an idea of how well it has performed over a long period of time, which is key in seeing how it manages the risks inherent in insurance underwriting.

Author’s presentation of 10K/10Q data

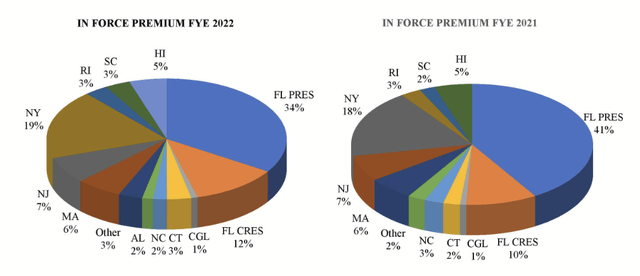

As described in the Dichotomy article, many people had hoped Heritage would see significant growth outside of Florida to diversify its risks. As evidenced by the rise in revenue over time, it has technically achieved that, but there is more to it than that.

Author’s presentation of 10K/10Q data

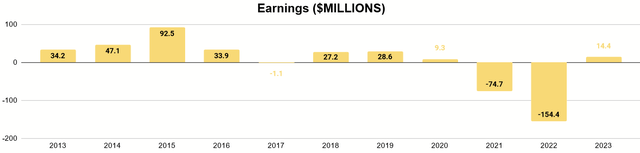

I did profits no It grows. In fact, they were their best in the first three years of this stretch (likely the reason Dichotomy was so optimistic in 2016). The trend turned towards losses that were heavy in 2021 and 2022. So what exactly happened here?

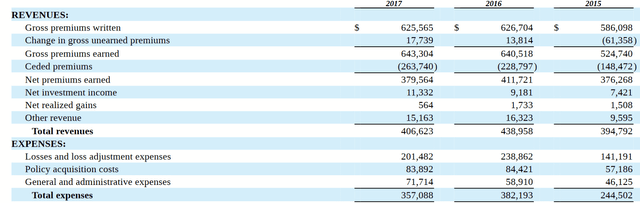

2017 10K model

As their income statement from 2017 shows, premiums ceded for reinsurance and loss expenses rose more than total premiums. In essence, the easy start described by the duo, with lower reinsurance costs, did not last. The company inevitably found itself doing business with a risk profile more typical of Florida. The financial situation was not helped by the financial impact of strong Hurricane Irma that year. Quoting from the 2017 10-K:

Total catastrophe losses associated with Hurricanes Hermine and Matthew were $21.8 million for the year ended December 31, 2016 and increased to $28.3 million as of December 31, 2017. The Company retained catastrophe losses associated with Hurricanes Hermine and Matthew in full. Huge disaster Losses associated with Hurricane Irma For the year ending December 31, 2017, it is estimated at About $560.0 million. Retained losses were $20 million under Heritage P&C’s reinsurance agreements with third parties.

Hurricanes Michael and Ian are also expected to hit in 2018 and 2022, incurring similarly huge costs.

The risk of storms to the Florida-based insurance business was one thing. The continued rise in demand for real estate there and thus the value of losses to be covered was another matter. The result is that claims payments grew at rates much faster than net premium income, hurting the bottom line and making Heritage an unprofitable underwriting insurer. Let’s take a look at the long-term impact on a company’s financial health.

Author’s presentation of 10K/10Q data

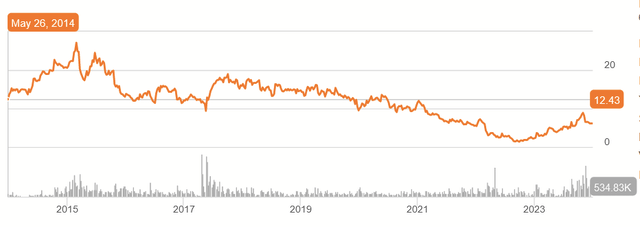

The company’s tangible book value, although rising for a while, is almost back where it started. However, if one looks at a stock chart, one will get a different impression of the company’s value.

Seeking alpha

What gives? The company has not been significantly diluted. In fact, until the recent sale of new shares, the company had been doing gradual buybacks. Why did the stock price fall to half of what it was at the IPO?

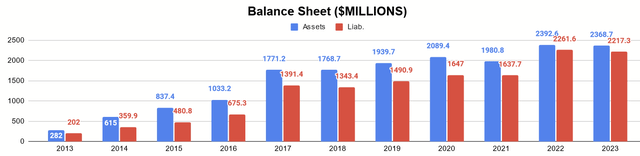

Author’s presentation of 10K/10Q data

Negative earnings and how they make investors feel about the future is one thing. The state of the balance sheet is another. As hardships accumulated, the gap between assets and liabilities narrowed. In 2014, buyers during the IPO acquired assets worth 70.9% above liabilities. As of Q3 2023, assets exceed liabilities by only 6.8%.

While the TBV for each stock is roughly the same, it is clear that the risks offered for that TBV are much higher.

A look to the future

Underwriting

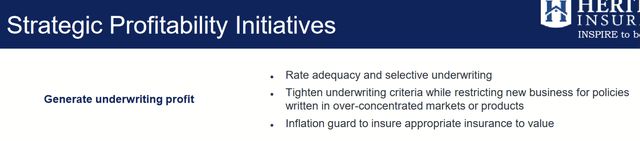

What are the prospects going forward? Well, management is aware of the conflicts.

Company presentation for the third quarter of 2023

One of their priorities is to run an insurance underwriting business profitably. Over the past few years, they have been working to turn this ship around.

Company presentation for the third quarter of 2023

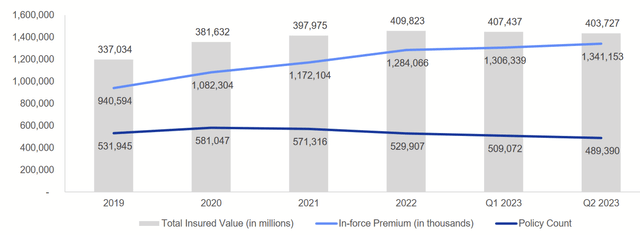

The number of policies in place fell from 581,000 to 489,000, which is a significant decrease. This strategy is also largely based on reducing exposure to Florida specifically.

2022 10K model

With year-to-date earnings through 2023 of $14.3 million, they’re barely moving toward profitability, but investors will want to keep an eye on a consistent trend. I think it will take a few years, at least, before enough consistent earnings are maintained to strengthen the balance sheet.

Investments

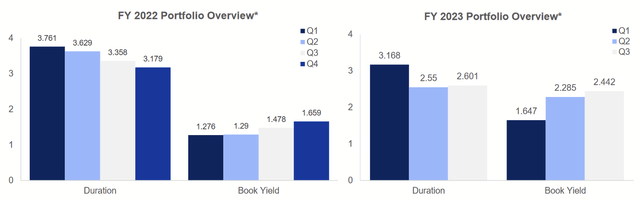

Beyond generating profits, a key part of the long-term value comes from Heritage’s investment portfolio. As mentioned before, this primarily concerns debt securities.

Company presentation for the third quarter of 2023

Most of these investments were of very short, medium to very low duration. Given the precarious state of the balance sheet, this may be wise, but the limits on the portfolio can be onerous, especially as the company becomes better off and benefits from increased equity investment.

The portfolio may grow as more profits are put into bonds, but its return will likely keep pace with inflation at best, given these low returns and the strict nature of its investment strategy.

Buybacks and dividends

If greater returns cannot be achieved through the portfolio, the company can still benefit shareholders by carefully distributing dividends or issuing buybacks. Given the concentrated negative impact of major storms, a regular dividend policy is likely not a welcome sign. I think the most reassuring sign would be occasional announcements of special earnings. Likewise, buybacks at a discount to TBV (which the company has done before) are welcome and better than dividends when the stock price falls. The recent share selloff I mentioned earlier, at a premium above TBV, also makes sense.

Only after a company has strengthened its balance sheet and has a risk model in place to make underwriting profits the norm, should a regular dividend policy be considered.

When is the purchase status?

Obviously, I think the company needs to improve its fundamentals further before I would buy at a price of around $6. To borrow terminology from Peter Lynch, this is a candidate for transformation. This type of insurance is also very cyclical in nature, as it will rise and fall as storms and other disasters cause property damage, a cycle that can be difficult to predict. However, in context, it can also be Play assets.

Seeking alpha

In late 2022, investors could have received a share price of less than $2. Naturally, the market was responding to the effects of hurricane season, but people who were following the company would have seen that it was at a discount compared to TBV:

Seeking alpha

While there are still some risks in this situation, there is more context for a happy ending. The first is that hurricane season comes and goes. Although he could return the following year, seasons don’t typically come in a 12-month Class 5 blitz and head straight to Florida. This gives the company some time to breathe. The lower it falls relative to TBV, the more attractive it also becomes as a takeover target by a better-capitalized insurer or conglomerate.

With TBV per share as of Q3 at $4.29, HRTG is trading at a premium. In essence, 2022’s asset players are in a position to finish on a positive note. This makes it easier to sell stocks in my opinion.

Conclusion

The company took off with massive tailwinds that made investors and even some analysts very bullish on the company. Once that money dissipated, oversubscription, followed by major hurricane strikes, destroyed profits and created a significantly weaker balance sheet.

Management is wise in dealing with these problems and has taken physical measures to improve the situation. However, it is still a work in progress and must be delivered before it is worth taking a stand. Meanwhile, a bad enough weather event on the East Coast could destroy the struggling heritage. Those who took a discount on TBV just a year ago now have a huge premium to exit. Given the risks, I think it’s a pretty easy sell. Investors can put their money into a profitable insurance company in the meantime.