bjayam/iStock via Getty Images

the iShares US Financial Services ETF (IYG) Covers US financial picks on a value-weighted basis. This means both insurance and banking. We have a view that inflation will continue to rise abruptly. We were made This point of view Clear For a few months in particular while the markets started pricing in deep discounts. In light of this, we see a mixed picture for IYG. While insurance may benefit, there may be more growing pain for banking companies that also participate equally in IYG. We prefer to veer into an insurance-focused portfolio.

IYG collapse

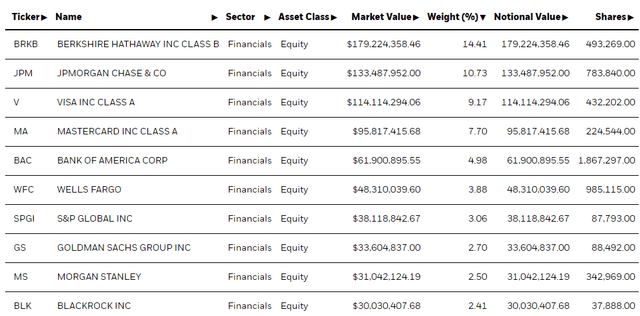

IYG consists of heavy exposure to Berkshire (BRK.A)(BRK.B), then JP Morgan (JPM), followed by some credit card picks as well as more full-service banks and rating agencies, with some asset management. also. On the whole, there seems to be much more than that Focus on banking rather than insurance Within IYG, with the only major insurance pick for the first two holdings pages being Berkshire.

IYG Top Holdings (iShares.com)

The P/E is over 16x, and the expense ratio is 0.4%, which is not great for a sector with a lot of market liquidity, with a theme that is easy to classify, however, according to FactSet data, it is still below the average of 0.6%. .

comments

Banking suffers slightly from the fact that most people in lending and deposits have been operating with portfolios that are exposed to unfavorable time lags. Simply put, they are forced to lend long and borrow short, and in a persistently low interest rate environment before coronavirus, this has led to a negative time lag that negatively exposes banks to higher interest rates.

This is not immediately visible, as deposit beta, which is how sensitive deposit interest rates are to changes in prevailing rates, does not kick in immediately, with increases in interest rates having to be observed as more or less sustainable. But now this is starting to happen and with competition from alternative financial institutions, deposit betas are likely to be higher than they were a decade ago. The banks are by no means in a dire situation, but seeing a decline in net interest income should be expected at this point. Ever-higher rates would make all of this progressively worse.

In insurance, it’s quite simple: Higher rates are great for insurers because they earn more from their reserve portfolios, which are heavily skewed toward fixed income. In the long term, they also offset higher costs of capital by achieving this performance in their large reserve portfolios.

The problem is that IYG has more banking than insurance, and with our concerns about the inflation battle, we don’t think IYG is a great pick.

minimum

We continue to see wage growth, and by the way we see strong employment numbers. It is crucial that US inflation expectations remain above 3%, and expectations fulfill the inflation prophecy. We confidently expect inflation will not decline, and view Powell’s comments as a greater concern for the final part of the Fed’s two-part mandate rather than the inflation component.

However, we believe that they will not ignore persistent inflation either because it will permanently cripple the Fed’s credibility, and that inflation will remain positively related to the interest rate position, even if growth becomes a concern for the Fed’s mandate. We do not believe interest rates will fall significantly as inflation remains at current levels.

We are seeing inflation continuing at significant rates in the US, and also in Europe, although European inflation is more or less independent of US inflation these days, as commodity price deflation affecting global markets has already occurred to a large extent.

A 16x PE does not provide much margin of safety, as dividend yields are only around 6%. Note that deposit and lending businesses may be more resilient than other components, especially for full-service banks, particularly investment banking and other transaction-based businesses, which may suffer from macro pressures as well as the potential for renewed uncertainty about costs of capital and inflation. . While the insurance exposures will do well, we feel that combined with the banking component, IYG does not look like excellent value to us, and its expense ratio of 0.4% is not insignificant given its 6.25% dividend yield.