Kamisuka

The tech sector’s reckoning (XLK) has arrived as we begin the first trading week of 2024. What looked like almost a market outperformance in December 2023 has hit late buyers hard. Retail FOMO fever peaked in late December Investors who failed to add exposure when Wall Street was extremely pessimistic will likely feel compelled to join.

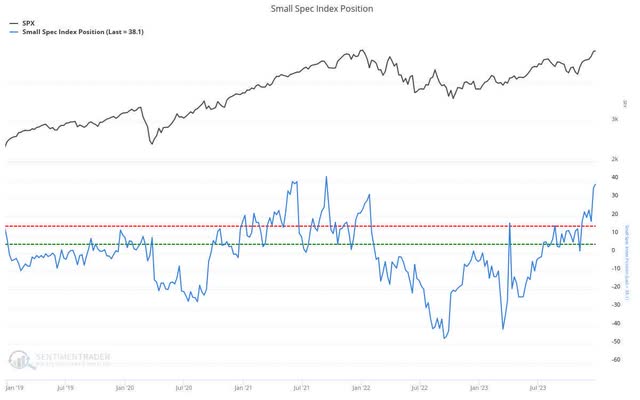

Small Speculators Index Position (Sundial Capital)

As a result, we recorded a remarkably high level of optimism among so-called “small speculators” or unannounced traders across the market at the end of December. The sentiment chart shows the net position of these small speculators “adjusted for position size and index value, expressed in billions of dollars.” It should be clear that December’s surge in bullish optimism peaked at superficial levels last seen in 2021. In other words, investors who chased technology in December The assembly asked for it: roads.

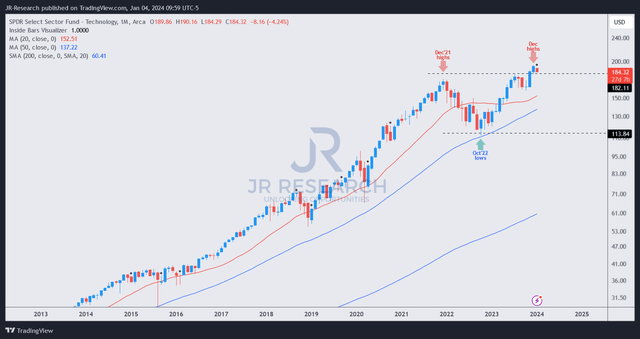

XLY Price Chart (Monthly, Long Term) (TradingView)

Based on XLK’s updated price action, most of the December gains have been lost this week (as of the January 4th trading session). However, since the above chart is a long-term XLK chart, we will only get the solution by the end of January. Therefore, the XLK Bulls are likely to remind us that it is still too early to indicate continued weakness, and they are right. However, it also emphasizes the importance of paying attention to price action and sentiment-driven metrics to assess risk/reward. Why? Is the technology sector generally overvalued? Yes. Based on Morningstar sector valuation estimates, the technology sector is overvalued by about 5%.

In other words, it’s not nearly as bubbly as the massively exaggerated levels in the 2020/21 pandemic bubble. However, interest rates are also much higher than those days, indicating a complex interplay as the market evaluates appropriate discount rates for technology stocks and growth stocks. The challenge is compounded by uncertainty about when the Fed could begin interest rate cuts in 2024. Therefore, fundamental investors are likely to face only complex scenarios that would have been simpler if they had a chart they could rely on while searching for… Strong stocks mainly for lower interest rates. It is considered.

I exited high-flying technology stocks at the end of December, as the meltdown presented me with several opportunities to do so. I will not discuss the details here out of respect for my members because they are provided in my service. However, one thing is for sure: I haven’t been adding to high-flying tech stocks lately. In contrast, the technology stocks I added included those that had reached peak pessimism, such as solar energy stocks.

With that in mind, I’ll present two of the top stocks for 2024 that I think readers should consider adding to their portfolios.

growth

First Solar Company (FSLR) It’s my favorite game to play in the potential recovery of solar stocks in 2024. Committed investors will likely recognize that higher interest rates, bloating inventory issues, and an industry-wide demand slowdown have weighed heavily on solar stocks in 2023. I’ve provided a more detailed thesis About FSLR in early December highlights why I believe FSLR is well poised to lead the recovery among its leading peers.

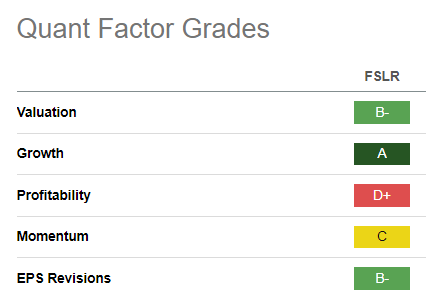

Quantitative FSLR scores (find alpha quantity)

Furthermore, FSLR was given a best-in-class Growth Score of ‘A’ and a Valuation Score of ‘B-‘, indicating a clear bifurcation of the growth stock. Market pessimism has created a great opportunity for investors keen to exploit this divergence, as the FSLR has outperformed the SPX significantly since my mid-December update. I think the opportunity is still relatively early, as solar stocks could make a strong comeback in 2024 as the market reevaluates the industry after a bruising 2023.

value

Investors in big pharmaceutical companies Pfizer (PFE) PFE had a ten-year round trip in December as it also reached peak pessimism. I also discussed this in an update in mid-December, suggesting why the market has finally been forced to capitulate in the long term. As a result, PFE lost all of its coronavirus gains and more, as the market downgraded PFE significantly. Therefore, it seems that the market has completely lost confidence in its COVID franchise as investors hastily exited to prevent further potential losses.

However, PFE bottomed out in December, as I expected. This week’s price action indicates that selling pressures have remained under control despite the broad market decline. As a result, I think the market must eventually realize that Pfizer is still a highly profitable pharmaceutical company (it has a best-in-class profitability grade of “A+”). Wall Street analysts expect Pfizer’s adjusted EPS growth distress to bottom out this year, which will reflect strongly on growth in 2024 (+48% YoY) and 2025 (+24% YoY). We’re not talking about long-term portfolio earnings accumulation, as those are measures of adjusted EPS growth over the next two years. With a FY25 adjusted EPS multiple of 10.4x (well below the 10-year average of 12.9x), the market has likely become too pessimistic about Pfizer’s execution of its earnings recovery.

He stays away

With retail investors recently focusing on high-flying technology stocks, I think the continued rotation could provide a harsh dose of reality for these investors. As investors keen to outperform, we must recognize market opportunities through potential sector or industry rotation before the rest of the market sees them.

Two of the stocks are featured above, and my members and I actually joined in, as the opportunity was just in time. I think investors looking to rotate their exposure from their hyper-tech and growth portfolio consider these two stocks to be my top picks for 2024.